Over the past few days at MORFO, we have been closely analysing the 2026 carbon market outlook published by Abatable. As a forest restoration implementer working daily with ARR developers, we sit at the exact intersection between capital expectations and field execution. When selection criteria shift, we see it immediately — in buyer questions, in investor hesitations, in projects that accelerate and others that stall.

The report does not focus only on ARR. It analyses the broader voluntary carbon market: demand dynamics, supply evolution, forward contracting, pricing curves, compliance convergence and integrity standards. But precisely because it takes a systemic view, it clarifies something fundamental for ARR developers: the market is not shrinking. It is concentrating.

Nature-based solutions attracted $9bn in funding in 2025. Forward carbon credit contracts reached $5.8bn, a 58% increase year-on-year. At the same time, compliance-linked demand is accelerating, with up to 78 million tonnes of additional CORSIA demand expected in 2026, on top of 58 million tonnes already required for 2024 emissions. Capital is available. But it is becoming more selective, more technical, and more structured.

Integrity is now the entry condition

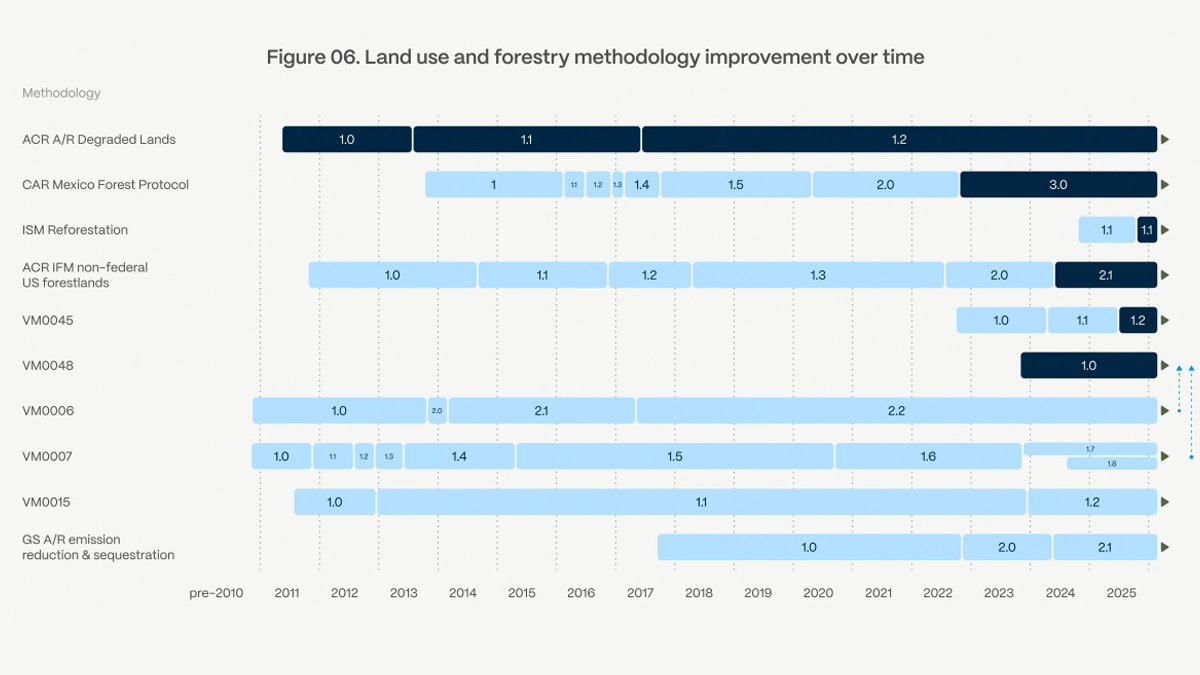

Around 40 methodologies are now recognised under CCP-level integrity frameworks. Projects developed under newly approved high-integrity methodologies could issue an additional 865 million credits by 2035, yet even with that projected growth, they would represent only 12.7% of cumulative supply by that date. This is structural scarcity at the top end of the quality spectrum.

For ARR developers, this changes positioning entirely. It is no longer enough to say a project is “high quality.” Buyers expect:

- Clear methodology versioning

- Explicit transition pathways toward newer standards

- Transparent permanence and leakage logic

- Structured governance and monitoring

Forward contracts are reshaping project economics

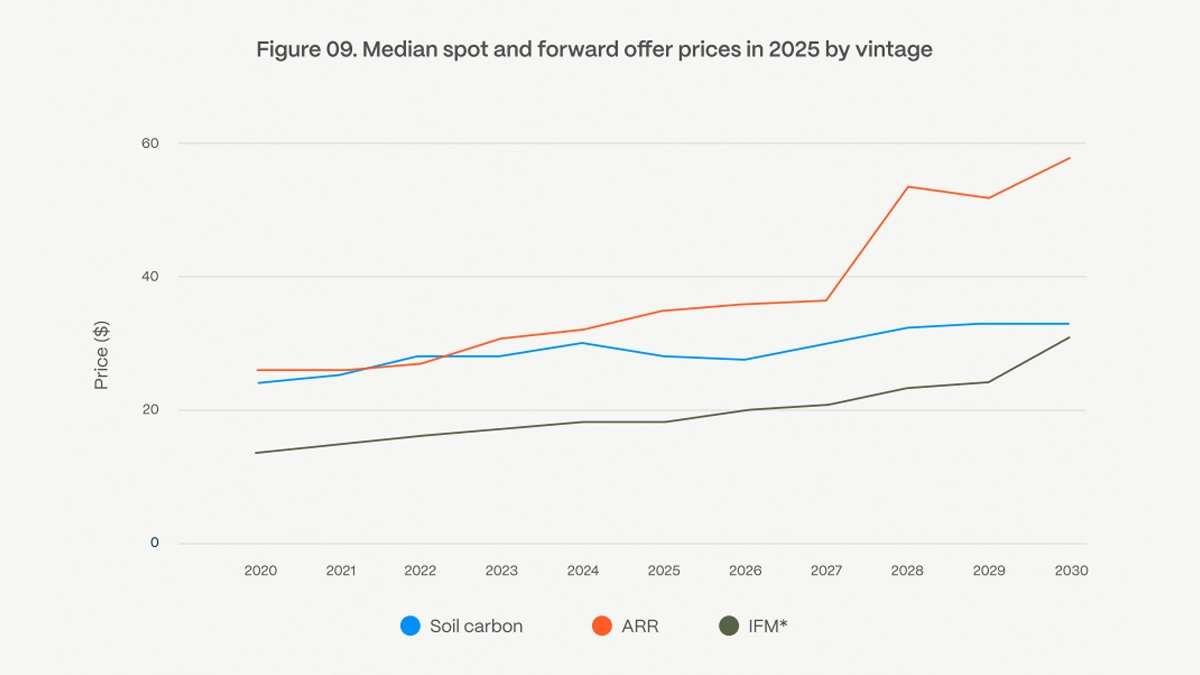

The sharp rise in forward contracting to $5.8bn in 2025 signals more than buyer appetite. It signals a structural shift in how carbon supply is financed. Buyers are no longer relying primarily on spot purchases; they are securing future vintages and underwriting methodology transitions. Forward price curves for nature-based removals, including ARR, rise significantly toward 2030. These increases reflect both scarcity and the cost of transitioning to higher-integrity frameworks.

For ARR developers, forward readiness becomes strategic. This requires credible issuance forecasts by vintage, transparent cost-of-capital assumptions, clear explanation of pricing evolution and milestone-based execution logic. Forward buyers are not simply purchasing tonnes; they are financing risk. Projects that cannot articulate how capital is deployed and how integrity upgrades affect pricing will struggle to secure long-term offtake agreements.

Compliance convergence is redefining demand

ARR projects are increasingly influenced by compliance mechanisms. CORSIA alone is generating structural demand measured in tens of millions of tonnes annually. Japan’s GX-ETS will allow companies covering 500–600 million tonnes of emissions per year to use credits for up to 10% of their obligations, potentially creating 50–60 million tonnes of annual credit demand. The convergence between voluntary and compliance markets introduces new layers of eligibility, authorization and governance requirements.

For developers, this means Article 6 readiness, host country alignment and vintage eligibility are no longer peripheral considerations. Projects that anticipate compliance-linked requirements and structure accordingly will access deeper pools of capital. ARR is gradually evolving from a purely voluntary instrument into a hybrid carbon infrastructure asset.

Buyers are institutionalising due diligence

Procurement mandates are becoming sharper and more technical. Buyers increasingly prioritise:

- CCP-approved methodologies

- Quantified co-benefits

- Recent vintages (often 2022+)

- Geographic and political stability

- Transparent pricing

For ARR developers, this translates into operational discipline. Permanence logic must be defensible. Biodiversity uplift must be measurable. Community revenue structures must be transparent and monitored. Buffer strategies must reflect regional risk. If these elements require excessive clarification or remain qualitative, projects will struggle to progress through institutional screening processes.

Co-benefits are moving from narrative to allocation logic

The rise of nature-related disclosure frameworks reinforces this shift. 620 organisations managing $20 trillion in assets have committed to TNFD-aligned reporting. Carbon portfolios are increasingly linked to broader sustainability objectives, including biodiversity and ecosystem resilience. As a result, ARR projects cannot compete on carbon alone.

Developers must quantify species diversity uplift, water system improvements, ecosystem resilience and local income generation. These metrics must be auditable and integrated into project governance. Co-benefits are no longer marketing additions; they are part of capital allocation logic in an increasingly institutional market.

What this confirms for ARR developers

This report does not introduce a new direction. It confirms the trajectory we have been working toward at MORFO over the past year. If capital is concentrating, projects must be structurally stronger from the outset. If forward contracts are becoming capital tools, execution must generate early visibility. If integrity is the entry ticket, design decisions must anticipate future methodology evolution.

Concretely, this is what we bring to ARR developers:

- Land intelligence before capital commitment. We assess more than 15 data layers per hectare before planting to remove weak hectares before they erode margins.

- Structured decision logic, not just planting. A/B/C zoning combined with Go / No-Go gates at M12, M24, M36 and M48 turns restoration into staged capital deployment.

- The right method per hectare. One project can combine multiple techniques, optimised hectare by hectare according to biophysical and financial logic.

- Visibility in 4–6 months, not years. With 3 cm drone imagery and AI-based seedling detection, we generate early performance signals and implement corrective actions within two weeks.

- Conservative carbon curves. We model downside scenarios first so that upside projections remain credible in institutional reviews.

The 2026 carbon market is not closing. It is professionalising. ARR projects designed as resilient carbon infrastructure — technically robust, financially structured and institutionally aligned — will access capital. Those built on generic assumptions and legacy positioning will face increasing friction.

The difference will not be in hectares planted. It will be in how projects are structured, monitored and financed from day one.